Helix Solar Group: A Case Study

It Was Never a Go-To-Market Problem — How a $35M Equity Check Quietly Became a Distressed Asset

The following is a composite case study drawn from a real engagement. Details have been modified to protect client confidentiality. The organizational dynamics, financial patterns, and outcomes described are accurate.

The Introduction

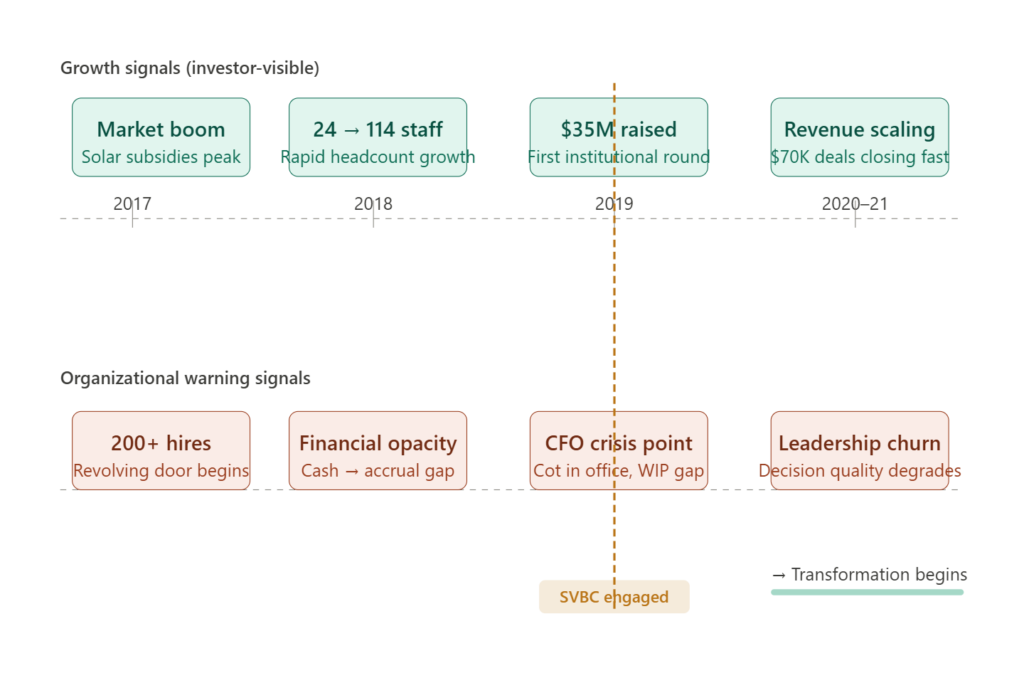

I was introduced to the leadership team at Helix Solar Group in Q3 2019, well before anyone was using the word “distressed” in the same sentence as their name.

The first thing I noticed wasn’t a spreadsheet or an org chart. It was the founder’s cufflinks. He’d just had a set of custom dress shirts made — seven or eight of them, if I’m remembering right — monogrammed at the cuff, following the close of their first institutional capital raise. He wore them well. He had the confidence of someone who had watched his father build a nine-figure construction company from the ground up, and had internalized every lesson that comes with that kind of proximity to ambition.

What brought me into the room wasn’t the founder, though. It was the CTO.

He pulled me aside before one of our early meetings and said something I’ve thought about many times since: “I’m excited about where we’re going. But I’m watching people leave faster than we can replace them, and nobody seems worried about it.”

That instinct — that uneasy feeling that the energy in the building was masking something structural — was exactly right. He just didn’t yet have the language to articulate what he was sensing, or a framework to diagnose it.

The Context: Solar’s Shining Moment

To understand what was happening inside Helix Solar, you have to understand what was happening outside of it.

This was the height of the residential solar boom. Federal subsidies were flowing. Consumer demand was surging. Getting solar panels on your roof wasn’t just an environmental statement — it was a financial one, and the industry had built an entire sales ecosystem around making that argument compellingly and quickly.

For companies like Helix Solar, the market wasn’t just favorable. It was intoxicating.

I remember one of their key leaders describing a habit that had become almost routine: he’d be driving on I-90, a sales rep on the phone with a live prospect somewhere across the metro, and he’d pull his car over on the shoulder to manually customize a solar layout in their proprietary software — real-time, from the highway — so the rep could close the deal before the client changed their mind. The rep would earn $1,500 on that install. Helix Solar would clear roughly $70,000.

“It was energizing,” he told me, with a grin that said he knew how that sounded.

That’s the thing about hyper-growth in a hot market. The wins are so large, so frequent, and so visible that they become the operating logic of the entire organization. Every problem feels solvable by selling more. Every gap feels temporary. Every alarm gets muted by the sound of the next deal closing.

What the Numbers Were Actually Saying

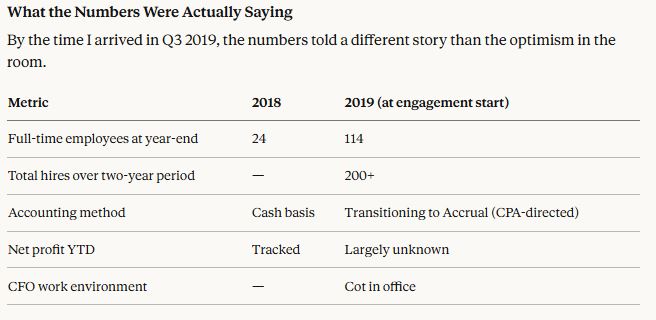

By the time I arrived in Q3 2019, the numbers told a different story than the optimism in the room.

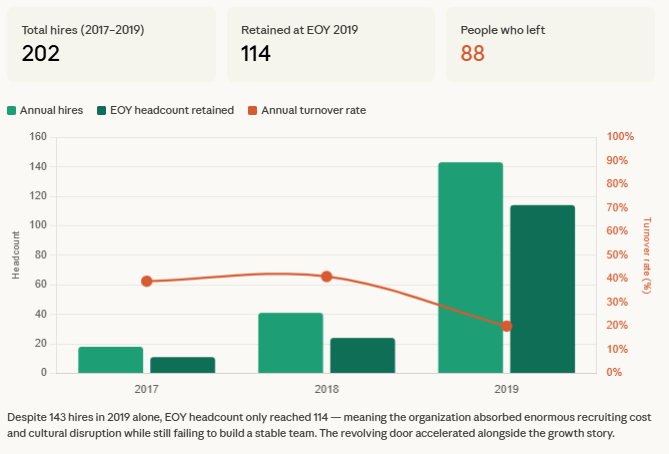

Let that sink in for a moment. A company that began 2018 with 24 employees had hired over 200 people in roughly two years — yet only retained 114 of them. That’s not a staffing strategy. That’s a revolving door with a recruiting budget attached to it.

Their CFO — a capable person by all accounts — had a cot in his office. Not a couch. A cot. He was sleeping there. He was trying to keep the WIP (work-in-progress) report current while simultaneously navigating a mid-year accounting method conversion from cash to accrual, which their CPA had correctly flagged as necessary for a company at their scale. The problem was that the transition had created a window of genuine financial opacity. Nobody could confidently tell you what their net profit was. Not the founder. Not the CFO. Not the board.

Meanwhile, their equity partners had written a $35 million check.

The Question I Always Get

“How does someone invest $35 million in a solar company without catching any of this?”

The honest answer: they saw what they were meant to see.

A founder with generational construction credibility and boundless conviction. A sales motion that was genuinely working. A market with federal wind at its back. Tantalizing top-line growth numbers on a deck that didn’t yet have to answer for margins, retention, or operational infrastructure.

This is not unusual. In high-growth sectors during favorable macro conditions, pattern-matching often wins over diligence. The signals that matter most — cultural cohesion, leadership capacity under pressure, organizational systems — are slow to surface in a traditional due diligence process. They show up in the hallways, in the turnover data, and in the behavior of people when the pace gets uncomfortable.

By the time a deal closes, those signals are often buried under momentum.

What I Found When I Looked Closely

After two preliminary meetings — and, notably, before my contract had even been signed — I was invited to their company holiday party at STK Chicago. That told me something. The founder liked having people in the room. He was a connector, a builder of energy. What he was less interested in was the machinery required to sustain that energy at scale.

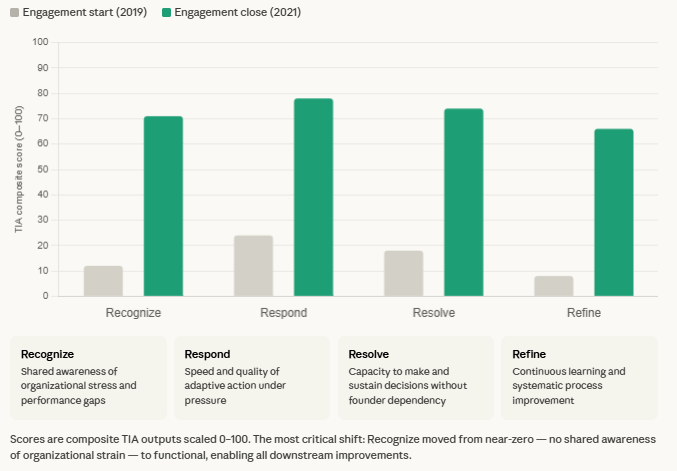

I began with what I call the SV Analysis — an open-response organizational assessment I had developed at that point (later formalized and expanded into the Trajectory Intelligence Assessment, or TIA). The goal wasn’t to generate a report. It was to understand two things: what the highest organizational priorities actually were, and how the leadership team had been responding to pressure — because that tells you far more about an organization’s health than any financial statement.

This highlights the organization’s capabilities in terms of how well the RECOGNIZE, RESPOND, RESOLVE, AND REFINE.

TIA’s 4R Capability Scorecard

From there, I moved into a deep-dive manual organizational analysis. I reviewed:

- Revenue architecture — how deals were structured, priced, and recorded

- Job costing — whether project-level profitability was being tracked, and what it revealed

- Hiring practices — who was making decisions, what criteria were being used, and how onboarding was structured

- Sales call monitoring — what the front-line selling culture actually looked like

- Organizational communication patterns — who had access to what information, and how decisions were being made under pressure

What I found was a company with a genuinely strong value proposition and a sales engine that worked — surrounded by an organizational infrastructure that had never been built to carry the weight being placed on it.

The growth had outpaced the systems. The systems had outpaced the people hired to run them. And the people hired to run them had never been given the time, the onboarding, or the stability to actually learn the job before the next wave of hiring diluted everything again.

This is what I now call execution drag — the invisible tax on organizational performance that accumulates when demands consistently outpace an organization’s capacity to respond, adapt, and sustain forward momentum. It doesn’t show up as a line item. It shows up as turnover, as financial opacity, as a CFO sleeping on a cot, as a founder pulling over on I-90 to personally rescue sales deals that his organization should have been equipped to handle without him.

The Transformation: Two Years of Deliberate Work

Over the course of the next two years, we rebuilt Helix Solar from the inside.

The work fell into several interconnected phases:

Phase 1: Diagnostic Clarity Before anything could be fixed, we had to establish a shared understanding of what was actually broken — and separate the structural problems from the circumstantial ones. The SV Analysis gave us a directional roadmap. The deeper organizational review filled in the details.

Phase 2: Revenue Architecture and KPI Development Their revenue model was working in practice but was not defined in principle. There were no clear KPIs. There was no consistent framework for measuring project-level profitability, sales performance, or operational throughput. We built that infrastructure. Once leadership could see what was actually driving margin — and what was quietly eroding it — decision-making improved almost immediately.

Phase 3: Operational Streamlining We systematically addressed the processes that had been built for a 24-person company and never updated for a 114-person one. Hiring practices, onboarding frameworks, job costing procedures, reporting cadences — each required a version of the same diagnosis: this was designed for a company that no longer exists.

Phase 4: Leadership Restructuring This was the most consequential and the most difficult work.

When mounting pressure degrades decision-making capacity, the most visible symptom is usually not the decisions themselves — it’s the people around the decision-maker. Leaders who had been stretched past their capacity, or who had been hired into roles they weren’t suited for, needed to be replaced. And the founder, for all of his vision and energy, needed to be repositioned.

By the end of the engagement, nearly the entire leadership team had turned over — deliberately, methodically, and in service of the company’s long-term health. The one exception was the CTO. His instincts had been right from the beginning. He stayed.

The founder was strongly encouraged — by his equity partners, and ultimately by the logic of the situation — to bring in a professionalized CEO and step into a thought leadership role. That’s not a failure. That’s what appropriate evolution looks like for a founder-led company that has crossed a certain threshold of organizational complexity. The hard part is getting everyone to the table before the asset is truly distressed.

What the Equity Partners Learned

When I eventually presented findings to the equity partners, they described their reaction as something close to relief. Not because the news was good — it wasn’t, entirely — but because they finally had clarity. They had invested $35 million into a story. What they needed was a diagnosis.

The revenue model was clarified. KPIs were established and tracked. The leadership team was rebuilt around people who had the capacity — and the stability — to perform at the level the business required. The financial reporting infrastructure, which had been held together largely by one exhausted CFO with a cot in his office, was professionalized.

What had quietly become a distressed asset was, over the course of two years, rebuilt into something that could sustain and grow the investment it had received.

What This Case Still Teaches Me

Looking back on Helix Solar, a few things stand out as true regardless of industry or market conditions.

Growth is not validation. A company can be adding customers, adding headcount, and adding revenue while quietly accumulating the organizational debt that will eventually collect itself with interest. The absence of crisis is not the presence of health.

Pressure reveals, it doesn’t create. Every dysfunction I found at Helix Solar had been present before the pressure arrived. The pressure didn’t build the problems — it surfaced them, accelerated them, and made them impossible to ignore. By the time they were impossible to ignore, they were also much more expensive to fix.

The founder is often the last to see it. This isn’t a character flaw. It’s almost a feature. The conviction that drives someone to build something is the same conviction that makes it difficult to accept that the organization they’ve built is under strain. Founders need people around them who can hold that tension — who are not cynics, but are also not captured by the founder’s narrative.

Due diligence has a cultural blind spot. The things that matter most in predicting long-term organizational performance — leadership capacity under pressure, cultural cohesion, the quality of decision-making when things get hard — are exactly the things that traditional financial diligence is least equipped to assess. That gap is where distressed assets are made.

The cufflinks were beautiful. The business needed different work.

Strategic Voyages Business Consultants (SVBC) works with growth-stage companies, PE-backed portfolio companies, and their leadership teams to identify and address execution drag before it becomes a capital problem. The Trajectory Intelligence Assessment (TIA) is SVBC’s proprietary diagnostic framework, grounded in Job Demands-Resources theory and the 4R organizational capability model.

{kind=link}

{kind=link}

{kind=link}

{kind=link}